Whenever you receive money – whether it’s a birthday gift from a family member or a pay cheque from a job – do you set aside some of that money to spend at some future date?

Whatever that goal is, the act of putting aside part of the money you receive is what is referred to as saving.

Getting into a savings habit is a fantastic starting point for you to reach your financial goals and build resiliency against uncertainty. It’s also an important step on the path to the responsible management of your finances, along with monitoring your expenses, paying down debts and creating a budget around your wants and needs.

Most people place their savings in savings accounts at a financial institution, such as Oaken Financial. In a savings account, your money is safe, easily accessible and covered by CDIC insurance up to applicable limits. It can even earn some interest.

For tax purposes, the two main types of savings accounts are registered savings accounts and non-registered savings accounts. The main difference between the two is that registered savings accounts, when opened within registered plans such as Tax-Free Savings Accounts (TFSAs) and Registered Retirement Savings Plans (RRSPs), have tax benefits. For example, within an RRSP, you defer taxes on your deposits and earnings until withdrawal. Within a TFSA plan, earnings are tax-free. However, registered savings accounts have annual contribution limits and other restrictions that Canada Revenue Agency may impose. Meanwhile, non-registered interest earning savings accounts don’t have tax benefits but are more flexible with deposit amounts and withdrawals.

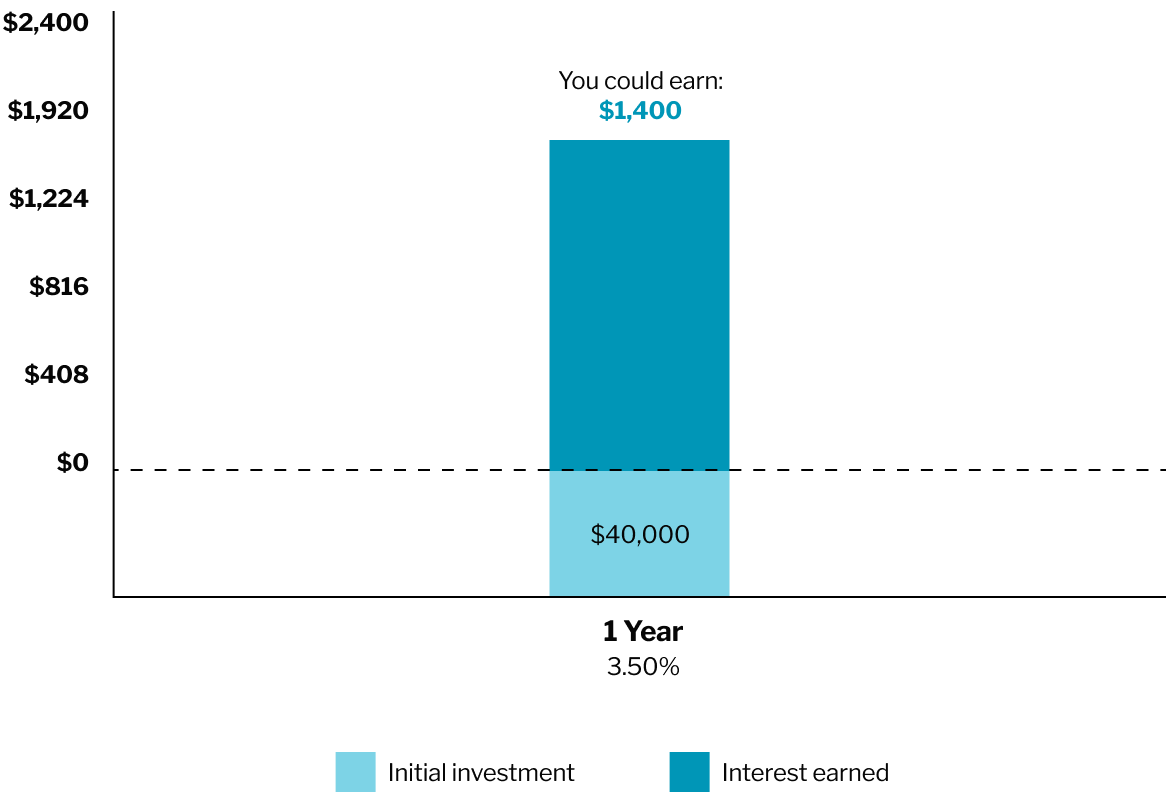

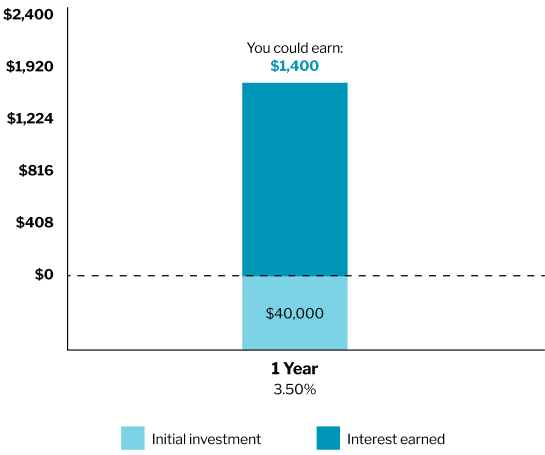

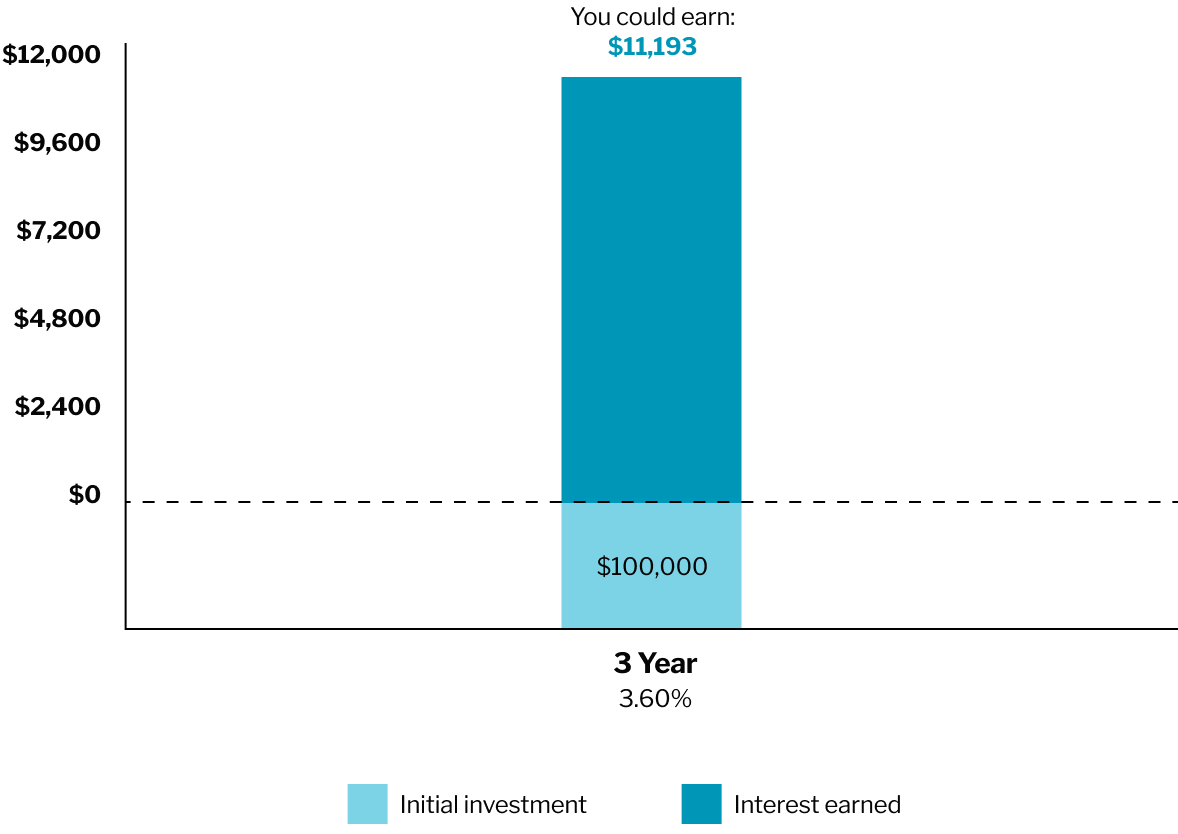

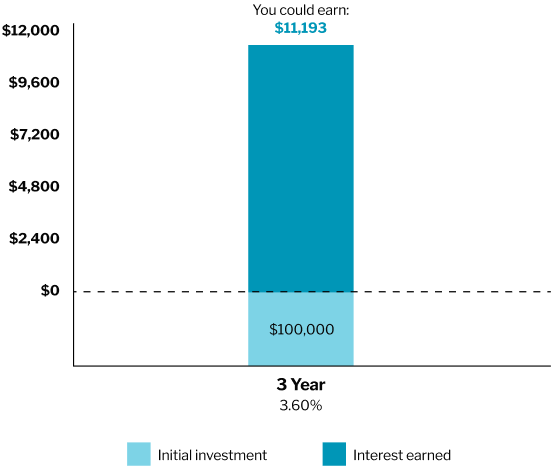

Making your money work for youIf you are saving for a long-term goal and want to earn more than the interest from a savings account, you’ll need to consider investing it. Investing is ideally for the money you won’t have an immediate need for.

According to the Financial Consumer Agency of Canada (FCAC), it’s important to figure out what savings and investments are right for you and to consider the following before investing your savings:

- Your financial situation

- Your financial goals

- How long you want to invest for

- Your risk tolerance